2025 State of the Sector

After several bruising years of disruption, the construction industry is starting to breathe again. The 2025 State of the Sector survey, which canvassed nearly 1,000 builders and homeowners, suggests that cautious optimism is replacing crisis mode.

72% of homeowners reported no significant delays with their builds. The most common causes of hold-ups recorded were largely beyond the builders’ control, namely delays in consent processing, supply chain constraints, subcontractor availability, and adverse weather.

“Homeowners are telling us that, even in challenging conditions, building in New Zealand can still be a rewarding experience,” Ankit Sharma, CEO of Master Builders, said.

He says the results show a sector that is resilient and professional, but still hindered by systemic issues. “These are promising results, and the sector should be proud.”

He noted that two-thirds had a positive journey, which speaks to the professionalism of Master Builders nationwide. “But we cannot be complacent, there are also areas where improvements can lift the sector further – faster consenting, clearer pricing, and stronger communication.

“If we get these fundamentals right, not only do projects move more smoothly, but trust and confidence in the whole sector grow.”

On budgets, the survey found that most projects were delivered on or under cost. Only 37% exceeded budget, typically due to changes in scope or design mid-project, unclear early estimates, or rising material prices.

Homeowners pointed to more detailed initial pricing, clarity around optional upgrades, early discussion of escalation clauses, and regular budget updates as ways to reduce cost overruns.

Momentous momentum

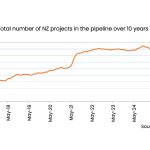

From the builders’ perspective, sentiment is gradually improving. 63% of builders believe the overall economy will improve within a year. 62% expect their own businesses to be doing better at the end of 2026 than they are now.

64% of builders reported strong or steady order books, up from 51% the previous year, while those facing a critical decline in work have dropped from 11% to 15%.

Yet conditions are uneven across the country; the South is rebounding more robustly, whereas Auckland and Wellington continue to face pressure.

“There are signs we are entering a new phase of the economic cycle,” Sharma says. “One that still carries risk, but also real momentum.

“Whilst the recovery is patchy, and we cannot overlook there are building companies across the country who are still finding things tough, however, there is a general sense that the building sector is shifting from surviving to delivering at a scale that secures the future and the country’s growth trajectory.”

Nevertheless, deep structural challenges persist, threatening industry growth. Chief among these is the rising cost of construction, which continues to be the greatest constraint on sector growth. Access to finance is another limiting factor.

More chronically, consenting delays seriously hamper productivity: many firms interact with more than one building consent authority (BCA), 72% say they’ve received “stop-the-clock” requests beyond statutory timeframes, and one in four have faced ten or more additional information requests before securing a Code Compliance Certificate.

“Builders and homeowners are telling us the same story: when consenting works, communication is clear, and finance is accessible, projects move faster, and experiences are better,” Sharma says.

“We’re ready to partner with Government, councils, and lenders to turn today’s cautious optimism into a sustained recovery.”